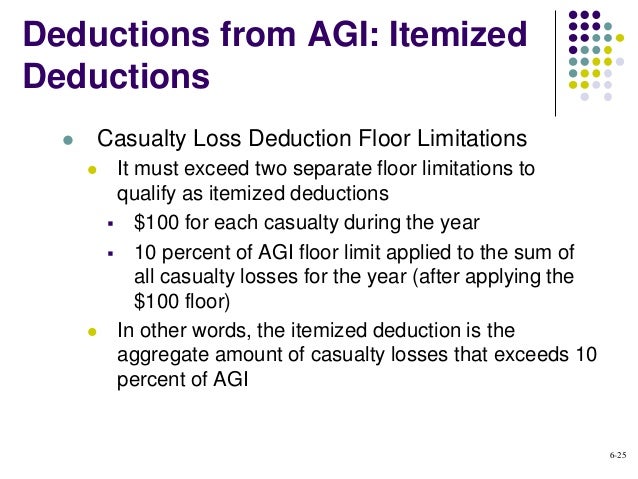

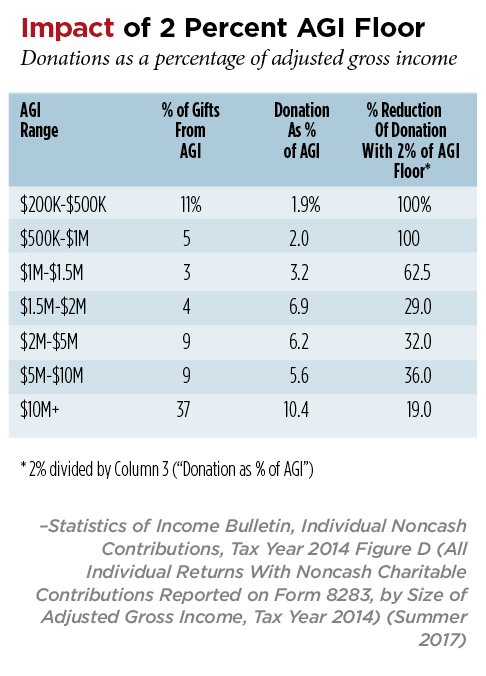

2 Percent Agi Floor

Acct321 Chapter 06

T09 0340 Medical Expense Deduction Floor Raised To 10 Percent Of Agi Baseline Current Law Distribution Of Federal Tax Change By Cash Income Level 2009 Tax Policy Center

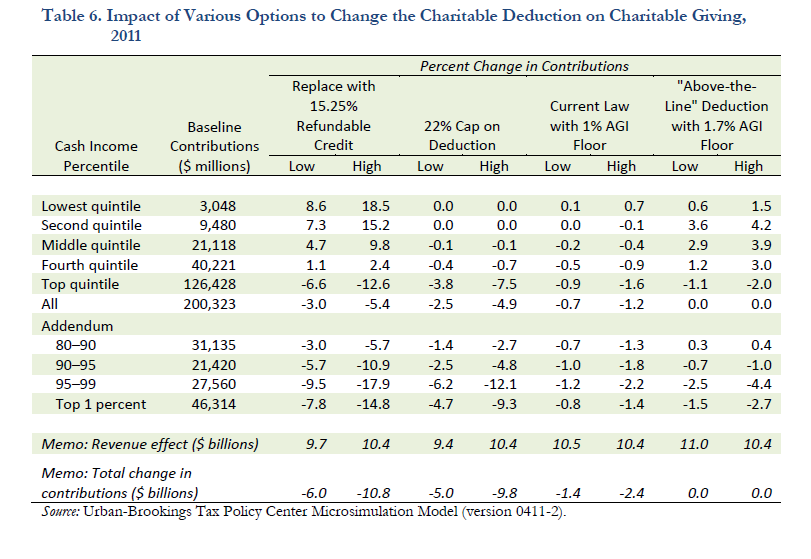

Options For Reforming The Charitable Deduction Committee For A Responsible Federal Budget

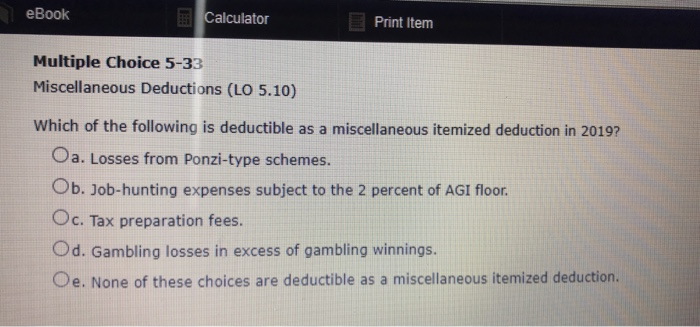

Solved Ebook Calculator Print Item Multiple Choice 5 33 M Chegg Com

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Gallery Of Candy Loft Studioac 12 In 2020 Loft Interiors Downtown Lofts House Home Magazine

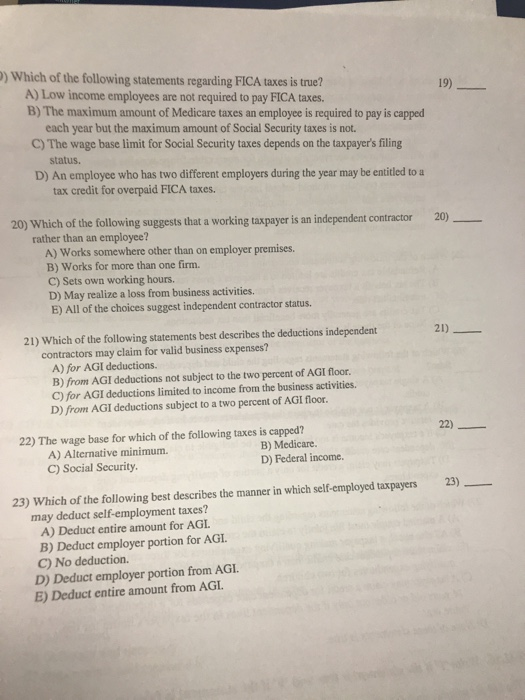

Subtract 2 of his agi from his deductions that are subject to the rule.

2 percent agi floor.

Pin On Interior Designer

Wayfinding Agi Open London Wayfinding Design Signage Design Directional Signage

Interactive Tax Forms

Tax Reform 2018 The Impact On Itemized Deductions For Individuals Jfs Wealth Advisors

Gallery Of Villa Tonden Hofmandujardin 16 In 2020 Modern Cabin Holiday Retreat Large Windows

Acc 555 Week 11 Final Exam Quiz By Goodm5474 Issuu

Solved Which Of The Following Is Relevant In Determining Chegg Com

Academic Onefile Document Individual Income Tax Rates And Shares 2005

Table 7 From Individual Income Tax Rates And Tax Shares 1 991 1992 60 Soi Income Concepts Semantic Scholar

Cfp Income Tax Planning Flashcards Quizlet

Photo 10 Of 15 In A Renovation Turns A Once Abandoned Barcelona Building Into An Airy Home From Yurikago Hous In 2020 House External Staircase Concrete Retaining Walls

Gale Academic Onefile Document Individual Income Tax Rates And Shares 1999

An Ultra Minimal Home In A Very Compact Space Japanese Style House Minimal Home Japanese Interior Design

Tax Deductions For Individuals A Summary Everycrsreport Com

Gallery Of Yun Shop Labotory 12 In 2020 Ceiling Design Interior Architecture Furniture Styles

Highlights Of The Tax Cuts Jobs Act Ppt Download

6917 Collins Ave 805 Miami Beach Fl 33141 Condos For Sale Miami Beach Collins

Brawell Landscape Mirror And Matching Items Matching Items In 2020 California King Bedding Furniture Vintage Bedroom Furniture

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gct56nogebssxibog0xr F694bnic C8pz25hgdcj0avumhwvno Usqp Cau

Maple Byparting Barn Doors Barn Doors Sliding Barn Door Barn Beams

Pdf Template Fursuit Head Base Canine Digital Download Etsy In 2020 Mandala Flower Mandala Mandala Wall Art

A New Tax Code Wealth Management

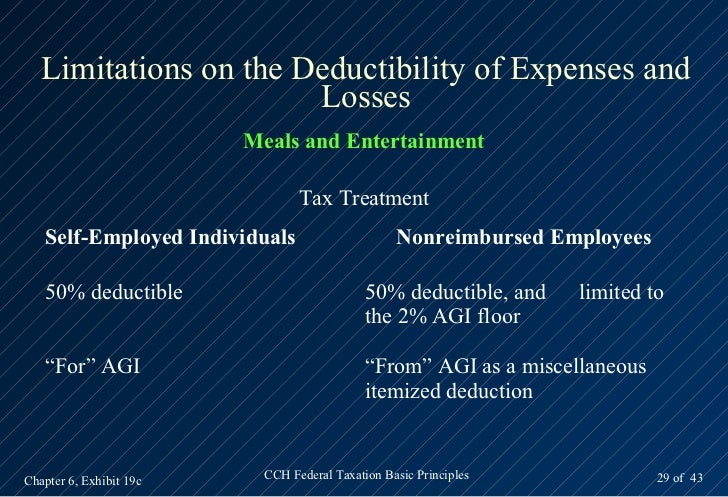

Chapter I7 Tax Deduction Expense

Gale Academic Onefile Document High Income Tax Returns For 2012

Video Agi Automatic O Ring Assembly Machine Press Forward Manufacturing O Ring

Tax Cuts And Jobs Act Individual Tax Planning Insight

Solved E False Write T If The Statement Is True And F Chegg Com

Webinar Slides Tax Reform S Impact On High Net Worth Individuals

Https Lawpracticecle Com Wp Content Uploads 2019 01 Lawpracticecle The New Tax Cuts And Jobs Act Pdf

Series From Tax Preparer To Financial Planner The Road Best Traveled Ppt Download

Federal Income Tax Laws That Cause Individuals Marginal And Statutory Tax Rates To Differ Sciencedirect

Ventura Poured Concrete Topping In 2020 Timber Feature Wall

Gale Academic Onefile Document Individual Income Tax Returns 1999

Gale Academic Onefile Document Individual Income Tax Returns 2011

2013 Cch Basic Principles Ch06

Fire Resistant Glass Pilkington Pilkington Pyrostop Provides Fire Protection Up To Class Ei 180 Available For Use With Miami Interiors Glass Pictures Design

Gale Academic Onefile Document Individual Income Tax Returns 2001

Fiorita Kornhaas Company Pc Newsletters

Acc 307 Technology Levels Snaptutorial Com

Interior Design Flat Prague Maisonette Loft Interior Luxury Interior Interior Design

Flexteam Sectional Couch Couch Home Decor

Healthcare Wayfinding Case Study Ucsf Medical Center Medical Center Wayfinding Interactive Kiosk

Customized Toughened Safety Architectural Tempered Glass For Building Laminated Glass Tempered Glass Glass Suppliers

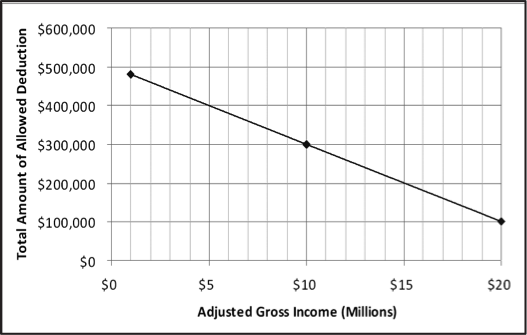

Deductibility Of Investment Advisory Expenses Impact Of Limitations Wealth Management

Source : pinterest.com